Britons are being urged to “plan carefully” for future debt repayments as interest rates rise to more than 35 percent, according to research by the Pew Research Center. Compare financial facts.

The average purchase annual percentage rate (APR) on credit cards rose from 34.7% at the beginning of March 2024 to 35.3% at the beginning of June 2024, according to the Treasury Department’s report on unsecured lending trends.

This number represents the highest level since Moneyfacts began recording this data in June 2006.

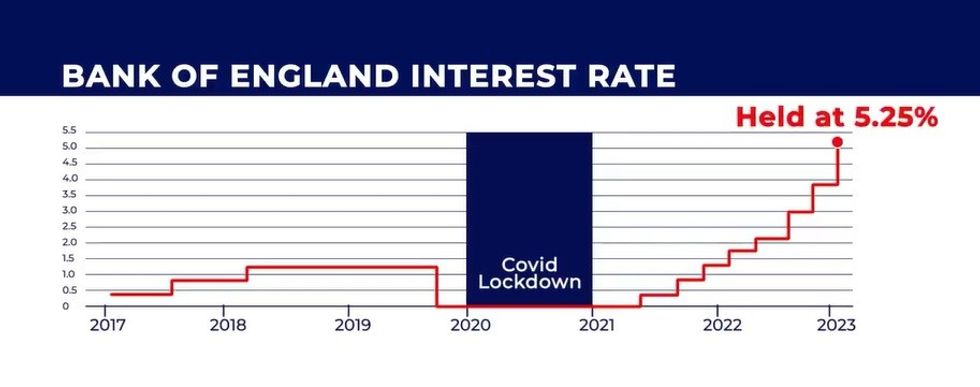

In recent years, interest rates on credit cards have risen in response to actions taken by the Bank of England.

The central bank’s monetary policy committee voted to raise the country’s key interest rate as it seeks to ease inflation.

As it stands, the bank has kept interest rates at 5.25 percent since August 2023 which has been passed on to savings and mortgage customers by the banks.

Do you have a financial story you’d like to share? Contact us via email money@gbnews.uk.

However, the interest charged on debt has increased significantly in recent years, as experts remind families to make their debt payments.

Many people choose to move their debt from an interest-charging credit card to a zero percent interest balance transfer card.

This can help families achieve significant savings, but the process of doing so has become increasingly expensive in recent years.

In June 2022, the average balance transfer fee remained at just 1.95%, later rising to 2.26% and 2.42%, respectively.

Rachel Springall, a financial expert at Moneyfacts, explains the dilemma many borrowers find themselves in.

She explained: “The cost of borrowing on credit cards has reached a record high, making it necessary for borrowers to pay off their debt if it bears interest, or convert it to an interest-free offer.

“However, the cost of transferring debt has also increased over the past quarter, and consumers looking for a zero percent purchase offer will find that product availability has stopped.

“The cost of living may lead some borrowers to turn to short-term credit, such as credit cards or overdrafts, but because of the interest cost, these credits should only be used temporarily to cover essential or unexpected expenses.

The finance expert cited research by UK Finance, which found that outstanding balances on credit card accounts grew by 9.5 per cent in the 12 months to February 2024.

With the number of zero balance transfer offers down by 100 per cent, she said providers are likely to be wary of this latest price hike and who remains in ongoing debt.

The latest developments:

The Bank of England has kept its key interest rate at its highest level in 16 years since it was raised to 5.25 percent last August. GB News

The Bank of England has kept its key interest rate at its highest level in 16 years since it was raised to 5.25 percent last August. GB News

“Borrowers will need to carefully plan their repayments to ensure they are in the best possible position to pay off their debts as soon as possible,” Springall added. “One way to do this quickly is to change the minimum repayment to a higher fixed amount each month, which can be changed again if the need arises.”

“An unsecured personal loan can be ideal for borrowers who want a fixed monthly repayment plan and know exactly when their debts will be repaid.

“However, the cost of borrowing £5,000 over three years has risen to its highest level in more than a decade. Borrowers will need to decide whether a loan is the right option compared to a more flexible credit card, but can seek advice if they are unsure.

“Seeking advice from a debt relief charity or seeking support from your current lender is always a wise idea to better manage your repayments and learn ways to avoid high interest charges.”